Written on: August 15, 2022 by Phillip J. Baratz

Picture this. You sold your customer a capped price of $2.99 per gallon for the winter. Your supplier sells you oil at a price of $2.00 per gallon on a day that the CME pricing (the “Merc”) is $1.90 per gallon. You turn around and sell it for a price of $2.99.

Then a few days later, the Merc is at $1.65 per gallon, but your supplier is still at $2.00 per gallon. You might frown, but you would pay $2.00 and sell it for $2.99. Then a few days later, the Merc is at $1.35 per gallon, but your supplier is still at $2.00 per gallon. You might frown even more, but you would pay $2.00 and sell it for $2.99.

The basis—effectively the spread between the Merc price and your supplier’s price (the “Rack”)—moved, but the customer just paid you your full margin. To a customer, the “basis” means nothing.

Now let’s turn that into the current reality. When dealers offer a price to a customer, capped or fixed, the calculation likely included:

*Merc price (fixed or capped)

*Basis (fixed or floating)

*Profit margin

For the past 10–15 years, the basis has not been a high item on people’s radar. Sure, it was always there, and sure there were ways to hedge it with suppliers or with a trading counterparty, but it was definitely a bit out of sight, out of mind. Companies fell into several categories relative to the basis:

1- Supplier-locked diffs at some point during the summer (with two subcategories)

a. Locked in for most/all of supply

b. Locked in for most/all of the program gallon supply

2- Hedged the basis via “paper” (i.e., a basis swap) leading up to the locking in of the supplier diffs

3- Didn’t hedge or lock the diff because they liked to shop around and didn’t find the basis to be a major concern

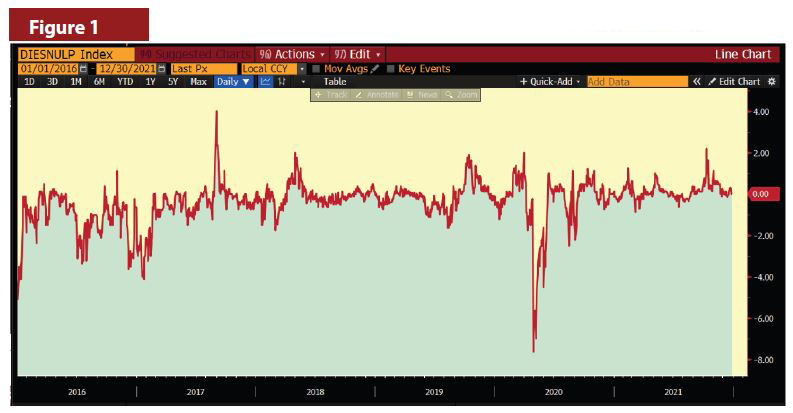

Basis versus Merc is somewhat akin to New York Harbor (the “Harbor”) versus Merc. Therefore, according to the “transitive law,” Rack versus Merc is similar to Harbor versus Merc. If there is a blowout in the Harbor versus the Merc, it will lead to a basis blowout at the rack. That is what happened this year, after spending years moving by only a relatively small amount—note the range from

-$.0750/gallon to +$.0400/gallon. Figure 1

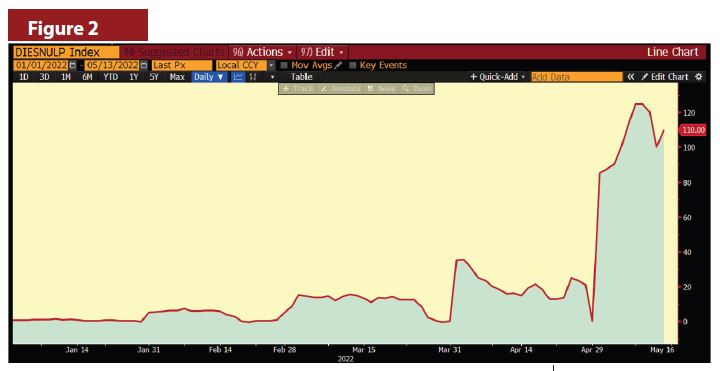

Russia then decided that it needed to attack Ukraine and jeopardize the world’s supply balance of oil, causing total disarray and a spike in the “near-term” pricing—and widening of the Harbor to Merc spreads. Note that since January, the spread range (which, over the five prior years was less than $0.12 cents/gallon), is now over $1.25/gallon. Figure 2

The basis blowout has caused program sales gallons to be delivered to customers in May at a net loss to dealers in many cases. Racks have remained somewhat steady with the Harbor, but the blowout between the Harbor and the Merc has led to some serious concerns and sleepless nights as we prepare for this coming year (and years into the future):

1- Will my supplier offer me a fixed-diff for next year?

2- If so, why are they telling me “Not yet?”

3- Also, if so, how high will that diff be?

4- If I haven’t considered locking in a diff, should I?

5- If I should, can I?

6- If I am nervous, is there another approach?

Root cause of blowouts

After studying the movements on the Merc, the Harbor and at the Racks, we believe that we have identified most of the root cause of the blowouts (in addition to suppliers just taking advantage of the situation, and there is nothing wrong with grabbing some extra money when it is available. Heating oil dealers do it all the time!)

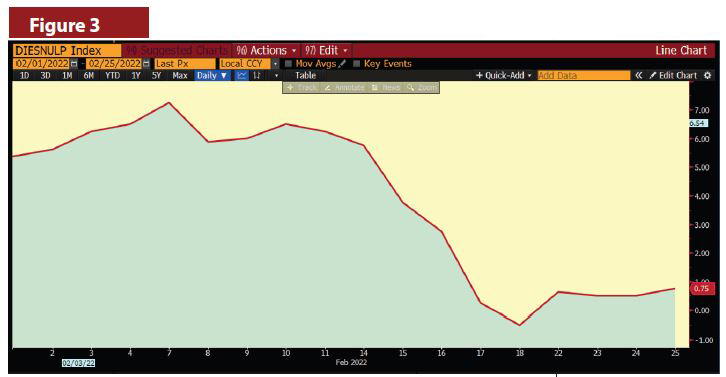

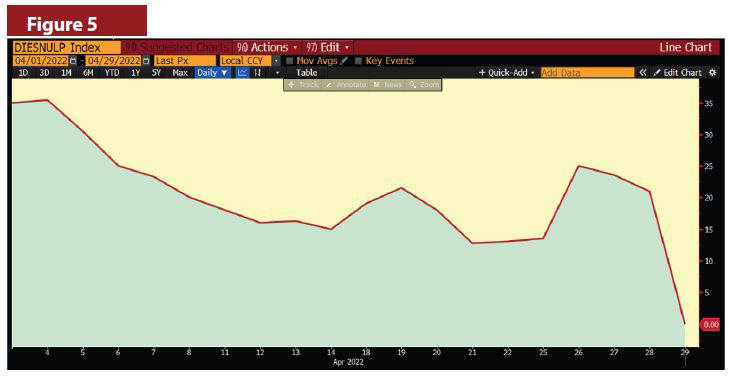

Combining two theories that we both believe are true, we believe a “proxy” exists to curb further basis blowout in the short-term and in total for next Winter. Theory 1 is that, as each month ebbs to a close, the cash market and futures market prices converge. That means that someone owning a futures contract at the end of the month can (technically) accept delivery of that product in the following month. Accordingly, the spread between the Harbor and the Merc tends to narrow down as the month comes to a close (see Figures 3, 4 and 5 focusing on February, March and April and how that diff narrows).

Theory 1 is that since the month ends with the basis pretty close to zero, but we are also seeing some wide Harbor to Merc spreads early in months (painfully so), the pain must be caused elsewhere. Theory 2 is that when the market senses that I need supply now, but in the following month things will be better than today (exactly what we witness in the current “backwardated” market), the spread between two futures contracts will have blown out.

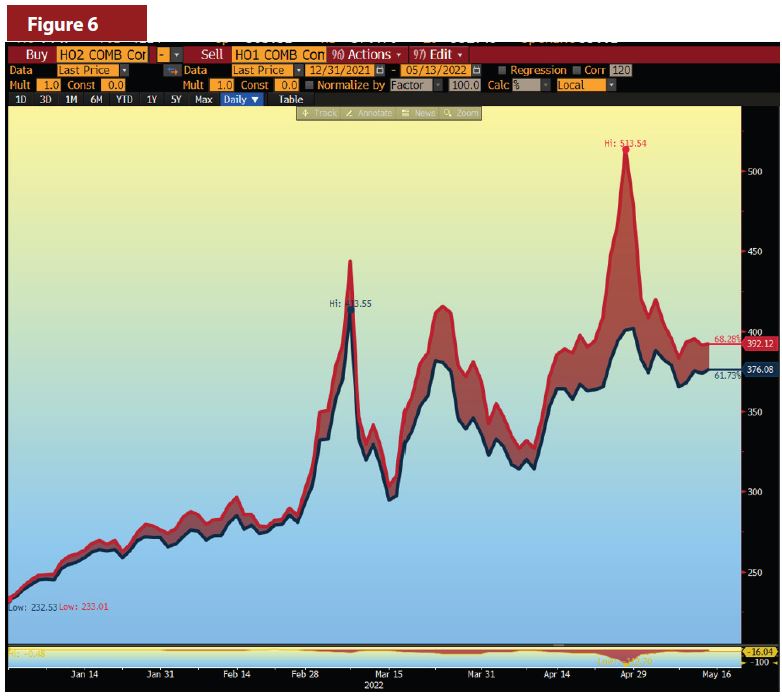

Figure 6 shows how those two contracts (Merc contract 1 and Merc contract 2) track each other and can become totally un-tethered.

A hedge plan may well address the basis blowout through a planned series of spread trades, if appropriate for you. We would assess the volumes that you plan to sell monthly, discuss the amounts that are subject to basis risk (in many cases it might be all gallons), compare the “what ifs” and make a hedging plan for your consideration. Leaving the basis spread as something that doesn’t matter is no longer a viable option.

Remember, customers don’t care about basis, but to you it might mean everything. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.