Written on: June 13, 2022 by Phillip J. Baratz

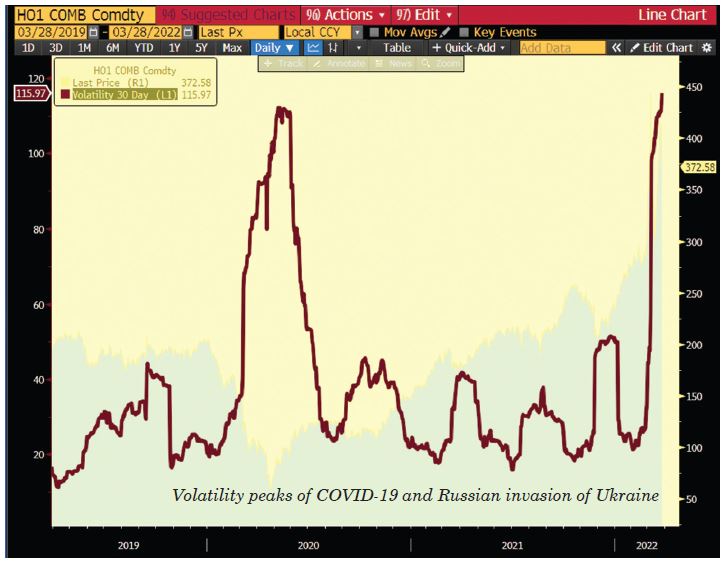

On the last day of 2021, the price of West Texas Intermediate (WTI) crude oil futures closed at $75/barrel (bbl). About 10 weeks later, the price had risen to over $90/bbl, and then just 10 days after that, prices traded over $130/bbl. In a 10-day period in February, ultra-low sulfur diesel (ULSD) futures rose from $2.85/gallon to over $4.50/gallon—an increase of more than 55%.

Industry veterans like to play it cool with pithy remarks about how prices always rise and fall, but eventually calm returns to the market. While that might be true, those veterans are likely not dealing with customers wondering why costs have jumped $2.00/gallon since their last delivery, or with banks and suppliers not willing to increase credit lines in the middle of Winter, nor with customers who don’t feel very motivated to pay a $900 oil bill in March when they won’t be due for their next delivery until September. Sure, calm might return to the market, but where does that leave you now and for next Winter?

Here are a few things we have seen & believe to be true:

Customers do not like surprises

For a reason that continues to confound all of us, customers seem to believe that:

A. Dealers make more money when prices rise and

B. Dealers wait until prices are high before making a delivery

Part of the solution to these two misconceptions is simple education of both your customers and your customer service representative (CSRs) in order to explain to your clientele. However, the notion of customers not liking surprises is completely limited to high prices. Customers like falling prices and they love low prices. You must educate them that you are on the same side as they are—you hope for low prices, but sometimes high prices are a reality. They also need to understand that sometimes prices swing uncontrollably (e.g., due to COVID-19, the Russian invasion of Ukraine, etc.).

Banks & suppliers like rules and can be rigid to deal with

Banks and suppliers are well aware that oil prices move. It is likely that they are following oil price gyrations much closer than you are. However, the credit lines they have set for you are dollar denominated, not “gallon denominated,” and the rules related to your credit are not that flexible.

If you have $1 million of credit and prices double, it will seem as if your credit has been cut in half—because it has! Unless you have a special relationship with the lender, changing terms in the middle of a crisis can be very difficult and potentially quite expensive. There are limits as to what you will be able to do to get more credit from lenders, but this should be another reminder that budget plans and pricing programs can be serious mitigators of cash-flow crises.

If you can’t control your margins, you can’t control your profits

This year, we witnessed an attitude among some dealers that they would and could “suck it up” and not increase sales prices in response to the spike at the rack. While that might seem noble, it is not your responsibility (unless you want to jeopardize your financial future).

Your automatic delivery customers agreed to pay whatever price you charge them for a delivery. That might work this year, but if your last delivery of the year is $2.00/gallon higher than the earlier deliveries, customers will remember that—and there will only be one place to point fingers (no, not the Kremlin nor the White House).

Achieving your per unit margin is what keeps you in business. Setting your pricing properly is the only way you achieve that. Additionally, as prices (and margins) sometimes seem uncontrollable, you must control your costs, other than what happens with the global price of oil. Basis and weather are often overlooked as risks, and usually do not cause major profit challenges, but when they do (e.g. basis blowout, frigid or balmy weather while prices are moving more than usual), the impact can be very large.

Pricing programs used to be “nice to have,” but no longer

If you do not offer a program, customers will (assuming they can afford to) pay your retail price. However, when those prices rise and fall wildly, it is not surprising that loyal customers are suddenly not so loyal. If you do not offer an alternative to “pay the market price,” someone else will. If you don’t think that customers are going to shop around for a Pricing Program after this Winters’ violent price swings, you may be in for a rude awakening.

Fixed prices are better than no program, but are too risky

Should prices fall precipitously between the time you lock in your customers and the next Winter rolls around, you might be facing some uncomfortable conversations. Customers will, undoubtedly, remember that you told them to lock in their price with you (while no such thing actually happened).

Our suggestion is to communicate all the rules regarding fixed prices, explain what happens if prices rise or fall, and if possible, this is the year to only sell fixed prices via a pre-payment. Yes, your customers are all credit-worthy, but trying to collect $5.50 per gallon if retail prices fall to $2.50/gallon might not be so easy. If you are going to offer a fixed price and you are getting pre-paid, you should be able to achieve your margin goals. However, offering fixed prices can lead to some serious retention challenges.

Capped prices establish a price ceiling, yet allow prices to fall

Capped prices are expensive! Let’s address the elephant in the room: the costs to hedge (generally through a strategy of options to cap prices) are higher than we have seen in a very long time, possibly ever. While you intuitively understand that, it can be hard to pull the trigger on buying the price protection. Is the timing right? What if prices fall tomorrow? Can I really charge or pass through such a high cost without losing customers? These are all real and valid questions.

If you think about it, you are doing something akin to buying hurricane insurance the year after a bad hurricane season. Sure, everyone wants and needs the insurance, but the premiums have jumped significantly. Our feeling is that you need to share your thinking with your customers. You didn’t cause the markets to fluctuate; you didn’t cause the cost of “insurance” to go up; and you are only there to help protect and service your customers in the best way you know how. The other part—which is part of a much more detailed discussion that you should have with your registered Trading Advisor—is trying to find the cost/benefit balance in setting your cap level, because the higher the cap, the less expensive the cost to put that cap in place. Is there a real difference to a customer between a cap of $4.50 versus $4.75? Maybe yes, maybe no. How much can you save by offering a higher cap? These questions, and more, must be part of the Advisory conversation.

Don’t panic

This March was an anomaly on a historical basis. Yet it did happen and we can only play the cards we are dealt. Next Winter’s prices are (as of this writing) cheaper than the prices we see today. Accordingly, you do have some flexibility in how you approach your pricing programs. More than anything, you need to plan, not spend your day guessing, hoping and reacting to things beyond your control.

Recap

You make money when you get full margins and when your customers stay with you. The only real way to have that happen is to carefully plan it out rather than “do what I did last year” and hope it works out for you. Understanding what you can and cannot control is the first step in getting where you need to be.

Price volatility, regulatory attacks on our industry, questionable abilities for customers to pay their bills and operating a business in a suboptimal way are our realities. Burying your head in the snow and hoping that the next generation will figure it out is not the right approach. Use the tools that are available, starting with the tool between your ears. Accept that you don’t know what will happen and accept that you can still do something about it. ICM

PAST RESULTS ARE NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

The risk of loss in trading commodity interests can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition. In considering whether to trade or to authorize someone else to trade for you, you should be aware that you could lose all or substantially all of your investment and may be liable for amounts well above your initial investment.